Wow, it’s been five years already. Five years ago it looked like the entire financial industry was about to collapse.

Major financial institutions, global banks, and hedge funds of assorted varieties went bankrupt. Companies like Bear Sterns, Washington Mutual and Lehman Brothers are no longer around. They either went out of business, or were acquired by other firms with assistance from the Federal Reserve.

The common thread was excessive leverage, and a lack of understanding of the underlying investments.

The resulting economic meltdown caused the biggest recession since the Great Depression, and a 43% decline in the S&P 500 (a broad index of the US stock market). Between March 2008 and February 2009, many investor portfolios that weren’t properly diversified across different asset classes saw declines of 50% or more.

Since then, the US economy has been slowly grinding forward. It no longer seems like we’re on the verge of economic collapse, but we’re not in a booming environment either.

Unemployment is still high (Forbes has a good article on why unemployment is higher than you think). The median household income, adjusted for inflation and seasonality, is 7% lower than it was in 2007.

But the US stock market has been on a tear and has achieved new highs several times this year. In the past 3 years, the S&P 500 is up 55%.

Some investors believe that the recent rise in stocks in not reflective of the current economic situation.

If you add the fear of rising interest rates to this mix, you wouldn’t be surprised if they though a sharp decline in the stock market is imminent.

And in fact, the stock market has drifted lower over the past weeks – rare for this year, although not uncommon for the month of August.

One question I’m frequently asked is whether it’s a good time to invest or not? I get asked this question, regardless whether the stock market is up or down, after all, there’s always something to worry about.

But this time, it’s prefaced with one scenario we haven’t seen for an entire generation – the real threat of rising interest rates.

“Stocks are at an all-time high, and interest rates are definitely going higher. The stock market is going to collapse. I’m scared about my future!”

What Happens To Stocks When Interest Rates Rise?

While history doesn’t always repeat itself, it often rhymes with the past. So let’s look back at the last time we were in a similar situation to see what happened to stocks.

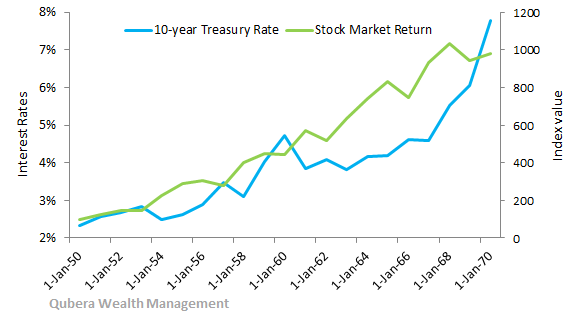

We have to look back a really long time – nearly 60 years.

Back in 1950 the Federal Reserve had manipulated interest rates to keep them artificially low and bottomed around 2.3% (not too far from where they are this time around).

But in 1955, the interest rates reversed their trend and started moving upwards. It wasn’t until 1969 (nearly 15 years) that interest rates hit 6%.

Between January 1st 1995 and December 31st 1969, the stock market had a compound annual return of 10.02%. (Note, compound annual return is the geometric return, and not the somewhat misleading simple average or arithmetic return which was 11.16%)

The last time interest rates went from 2.7% to 6%, the stock market went up four-fold!

Were stocks much cheaper in 1955 than they are today? Not really.

In 1954, the stock market rose 56%, and by 1955 stocks were trading a Price/Earnings multiple of 13. We’re currently trading at a P/E of 16, and if you believe 2014 estimates then we’re only at a P/E of 14.

And if you’re investing in a globally diversified portfolio, you’ll be buying international as well as emerging market stocks – all of which are currently cheaper than they’ve been in the past few years.

A lot of my favorite large-cap dividend-paying international stocks are trading at P/E multiples between 9 and 12.

Prudent investors buy stocks when the P/E is historically low.

So while no one can reliably predict the future, I expect the future long-term returns of a well-balanced and globally diversified portfolio to be quite good. We might see some ups and downs, but we’re still a long way away from being ridiculously over-valued.

Sticking to your predetermined investment plan regardless of short-term events is the best way of reaching your long-term goals. As always, keep calm and carry on!