Today was a historic day for the Dow Jones Index – and a harrowing day for investors. The blue chip stock index fell 1,089 points, the biggest intraday move in the history the index, before recovering to a loss of only 588.

Over the past three months, the S&P 500 has dropped about 7.5%. There hasn’t really been any safe haven as global markets have dropped as well.

Except for bonds, every other asset class is down for the year to some extent. The biggest losers have been Emerging Markets and Commodities, down 19% and 22% year-to-date.

Today’s action was the culmination of what’s been an incredibly bad week for the global markets.

The S&P 500 is now down 10% from the peak this year, and is officially in a correction.

As I mentioned in my last post, we were anticipating a 10% or even a 20% decline sometime in the near future.

On average, the market drops 10% about once a year. However, we’ve gone 4 years without this sort of correction – it was only a matter of time before the market dropped.

And, as usual, the news outlets are full of doom and gloom articles predicting the end of the world. After all, bad news sells.

But you shouldn’t worry too much about a decline of this magnitude.

Unlike 2008, we’re not on the verge of a major recession, nor are the financial institutions on the verge of collapse (at least not yet!). The current environment is not similar to 2000 either, where technology stocks were ridiculously overvalued, and the overall stock market was twice as expensive as it is today.

Today’s market is fairly valued, trading at a P/E of 18.

The P/E or Price-to-Earnings ratio denotes how much someone is willing to pay for a dollar of earnings. A P/E of 18 means investors are willing to pay 18 times earnings. 18 times earnings is a fairly valued market. Above 25 it’s getting expensive. Above 35 and you should be extremely cautious.

Sometimes investors get caught up in the euphoria of owning stocks, and are willing to pay any price.

This is the scenario that recently unfolded in China.

The Shanghai Composite Index soared 133% in the past year until it was trading for over 40 times earnings. This year alone, it was up 60% at the peak before eventually crashing. Instead of being up 60%, it’s now down 1% for the year.

A lot of ordinary middle-class Chinese investors got hurt, speculating in something they didn’t understand. Just like in the US stock market 15 years ago, and the US housing market 7 years ago.

But we’re nowhere close that level of frothiness in the US markets today.

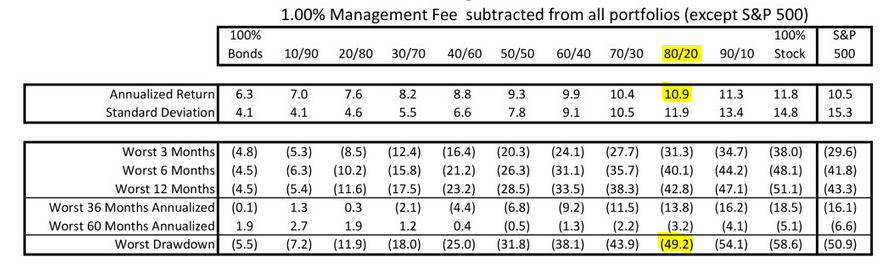

Over the past several decades a well-diversified global portfolio with 80% equities and 20% bonds has returned between 9-11% over any 20 year period.

(Click to Enlarge)

source: http://paulmerriman.com/fine-tuning-asset-allocation-2015/

However, there have been very few years during the entire timeframe when the portfolio actually delivered 9-11% in any given year. We either see 11%+ returns (such as 2013, when this 80/20 portfolio returned about 15%) or below 9% returns (like 2014 when this 80/20 portfolio returned about 3%).

And there will be times when your account has negative returns. Maybe for a few years in a row.

Over your investment lifetime, there will be at least one or two periods when your portfolio will drop 25% or more (as it did in 2008). Despite these huge declines, the nature of the markets and compound interest will ensure a high probably of achieving satisfactory results. So long as you don’t panic and bail at the bottom of the market.

This is easier said than done. Imagine if you had several hundred thousand dollars in your account and you’d just lost $200,000. In this situation most people cry uncle and change their investment strategy.

Don’t let these short term drops in the market upset you, and derail your investment plans.

In fact, you should pray for a severe and protracted bear market so you can keep buying stocks at a cheap price.

Remember, when the price of stocks fall, they become less expensive and also less risky. However, the stock market is the only market where investors flee when they see a bargain!

The only time you’d hate these huge drawdowns in your portfolio is when you’re close to, or in retirement. But, your asset allocation should have already been modified to adjust for this, and your exposure to stocks would have declined in favor of bonds. This lowered exposure to stocks would have helped moderate the losses in your portfolio.

You’ve probably heard stories of older investors who lost 50-60% of their 401ks in 2008 and had to either put off retirement or go back to work.

These are the people who didn’t have the proper asset allocation, and had too much exposure to stocks, or volatile asset classes like REITs, commodities or small-cap stocks. The difference between a portfolio that has 60% in equities and one with 90% equities is the difference between losing 35%, and losing 55%.

A 35% loss stings, but a 55% loss results in sheer panic.

And when people panic, they tend to behave in a manner that is injurious to their health, or in this case, their long-term financial well-being.

I personally know several investors whose portfolios lost 50-75% of their value in 2008/2009 and they moved everything to cash.

Some of them are still in cash.

Meanwhile, the S&P 500 is up just over 200% since the bottom in 2009. Compared to that increase, this 10-20% loss is minor blip. As in 2008 and 2009, staying in the market through this turmoil may prove to be a very wise move.

If you have a long-term horizon, don’t let short-term events derail your investment plans. If anything, see them as an opportunity to buy stocks at a discount.

We’ve taken this opportunity in the markets to rebalance our client portfolios. In a bull market, this strategy forces you to take profits along the way. In a correction, it makes you buy back some of the assets that have dropped in price. In effect, this time-tested strategy takes a lot of the emotions out of our investment process and forces us to sell high and buy low.

Stay the course.